38 duration for zero coupon bond

What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... Mr. Tee is looking to purchase a zero-coupon bond with a face value of $50 and 5 years till maturity. The interest rate on the bond is 2% and will be compounded semi-annually. ... Therefore, it might be profitable for the bondholder in the case of a long duration (a higher 'N'). Disadvantages of Zero-Coupon Bonds. What Is the Difference Between a Zero-Coupon Bond and a Regular Bond? Zero-coupon bonds may also appeal to investors looking to pass on wealth to their heirs. If a bond selling for $2,000 is received as a gift, it only uses $2,000 of the yearly gift tax...

dqydj.com › zero-coupon-bond-calculatorZero Coupon Bond Calculator – What is the Market Price ... P: The par or face value of the zero coupon bond; r: The interest rate of the bond; t: The time to maturity of the bond; Zero Coupon Bond Pricing Example. Let's walk through an example zero coupon bond pricing calculation for the default inputs in the tool. Face value: $1000; Interest Rate: 10%; Time to Maturity: 10 Years, 0 Months ...

Duration for zero coupon bond

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value. Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep If the zero-coupon bond compounds semi-annually, the number of years until maturity must be multiplied by two to arrive at the total number of compounding periods (t). Formula Price of Bond (PV) = FV / (1 + r) ^ t Where: PV = Present Value FV = Future Value r = Yield-to-Maturity (YTM) t = Number of Compounding Periods Convexity of a Bond | Formula | Duration | Calculation - WallStreetMojo The duration of the zero-coupon bond which is equal to its maturity (as there is only one cash flow) and hence its convexity is very high While the duration of the zero-coupon bond portfolio can be adjusted as to that of a single zero-coupon bond by varying the nominal and maturity value of the zero-coupon bonds within the portfolio.

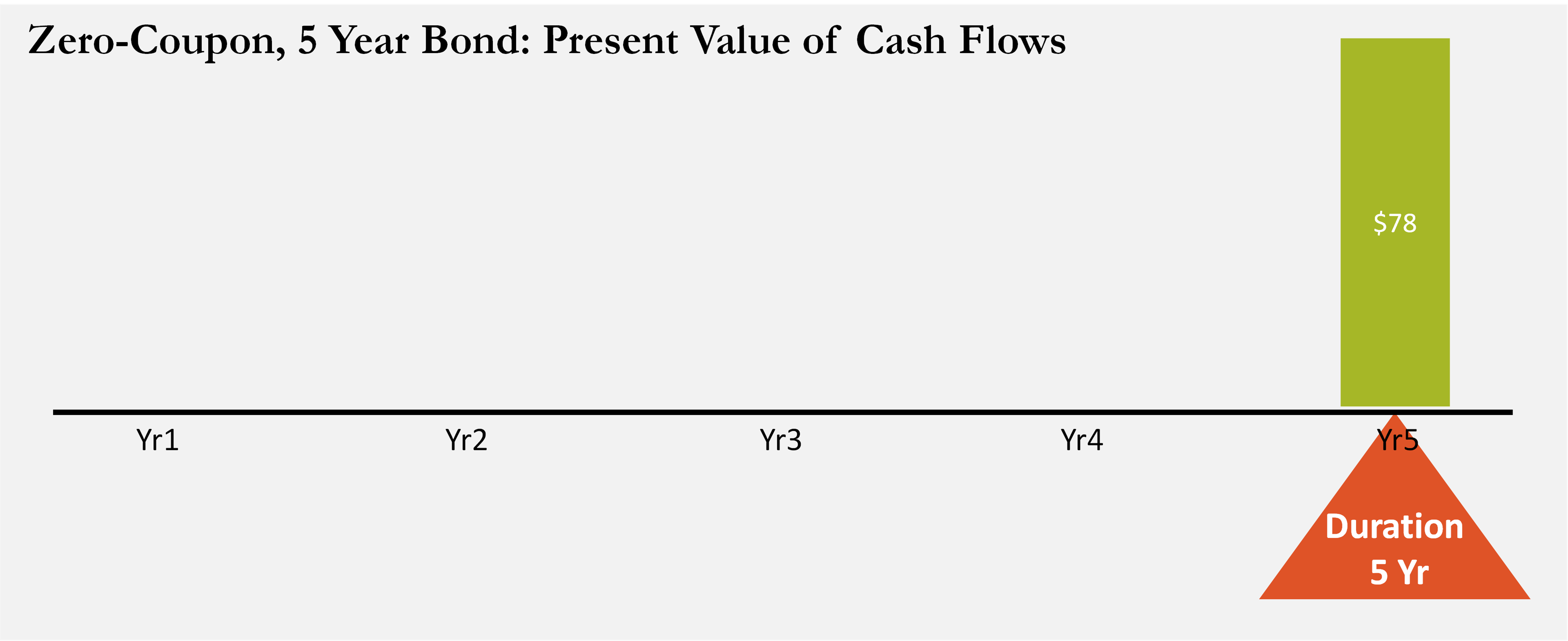

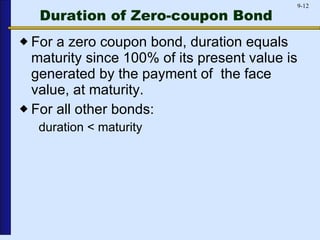

Duration for zero coupon bond. Zero-coupon bond - Wikipedia Zero coupon bonds may be long or short-term investments. Long-term zero coupon maturity dates typically start at ten to fifteen years. The bonds can be held until maturity or sold on secondary bond markets. Short-term zero coupon bonds generally have maturities of less than one year and are called bills. › terms › dDuration Definition and Its Use in Fixed Income Investing Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ... › fixed-income-bonds › durationDuration: Understanding the relationship between bond prices ... That said, the maturity date of a bond is one of the key components in figuring duration, as is the bond's coupon rate. In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. When a coupon is added to the bond, however, the bond's duration number will always be less than the maturity date. duration of zero coupon bonds | Forum | Bionic Turtle With respect to a zero coupon bond, Macaulay duration = maturity, and therefore must be a monotonically increasing function of maturity. On the other hand, DV01 of a zero (or deeply discounted) is not strictly increasing as DV01 = P*D/10,000 and the numerator has offsetting effects. If you'd kindly reference, I can fix? Thanks! Apr 7, 2012 #3 S

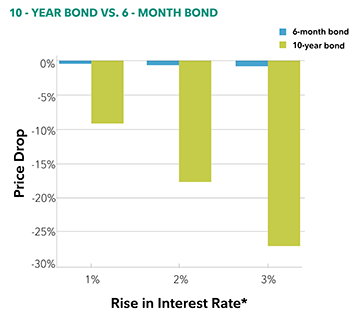

› articles › bondsDuration and Convexity to Measure Bond Risk - Investopedia Jun 22, 2022 · The duration of a zero-coupon bond equals time to maturity. Holding maturity constant, a bond's duration is lower when the coupon rate is higher, because of the impact of early higher coupon payments. › stories › memberpageLiterotica.com - Members - SZENSEI - Submissions Mar 08, 2017 · Starting from Scratch Ep. 021: ZERO G (4.65) What goes up must cum down. Spewton's Law! Exhibitionist & Voyeur 08/31/20: Starting from Scratch Ep. 022: YOOHOO OVERHEAR (4.66) Piper dances with the Wolfman. His class howls at her moon. History in the shaking, General Lee speaking. Exhibitionist & Voyeur 09/07/20 How to Calculate Bond Duration - wikiHow Duration is measured in years, so your final answer is 2.914 years. 9 Use Macaulay duration. Macaulay duration can be used to calculate the effect that a change in interest rates would have on your bond's market price. There is a direct relationship between bond price and interest rates, mediated by the bond's duration. Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

What is the duration of a zero coupon bond? - Quora Originally Answered: what is the duration of a zero coupon bond? Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. Zero Coupon Bond Modified Duration Formula - Bionic Turtle We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%. Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding Zero Coupon Bond Calculator - MiniWebtool The zero-coupon bond value calculation formula is as follows: Zero coupon bond value = F / (1 + r) t. Where: F = face value of bond. r = rate or yield. t = time to maturity.

How to Calculate PV of a Different Bond Type With Excel

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

Modified Duration - Zero Coupon Bond Modified Duration ...

› arena › what-is-bond-durationWhat Is Bond Duration? Definition, Formula & Examples Oct 03, 2022 · In the world of bonds, "duration" does not mean timeframe ...

Macaulay Duration

Understanding the Relationship Between Coupon Rates and Duration For example, if I purchase a zero-coupon bond on its issue date the bond will have a duration of 30 years - no cash flow until the bond matures. If I purchased a bond with a 6% coupon rate, duration would be significantly less than 30 years because I'm receiving semi-annual bond interest until the bond matures.

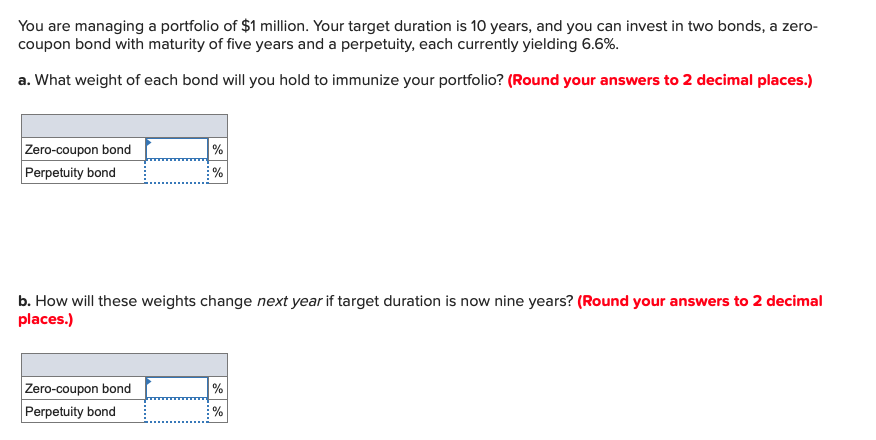

Solved] You are managing a portfolio of $3.0 million. Your ...

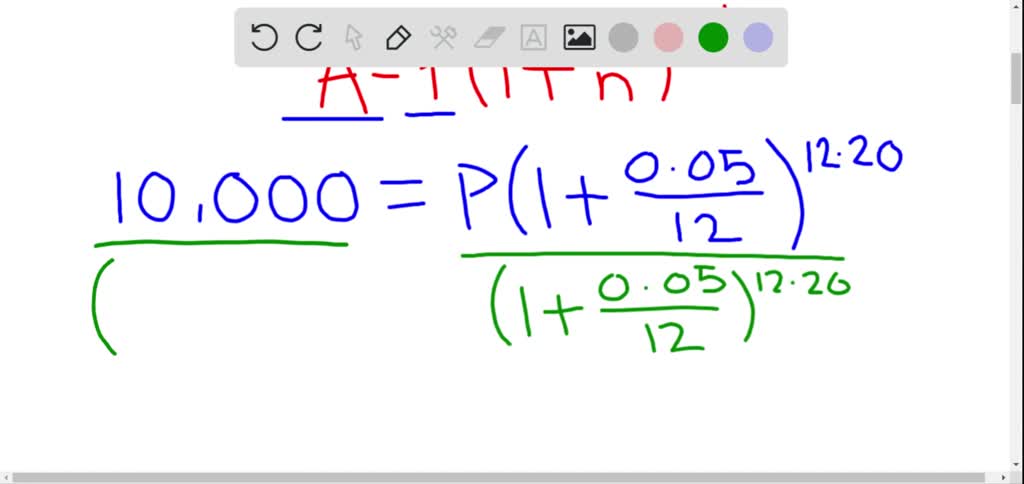

The Macaulay Duration of a Zero-Coupon Bond in Excel - Investopedia Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

Bond Duration Calculator - Macaulay and Modified Duration - DQYDJ From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity - it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

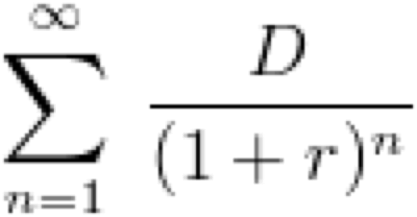

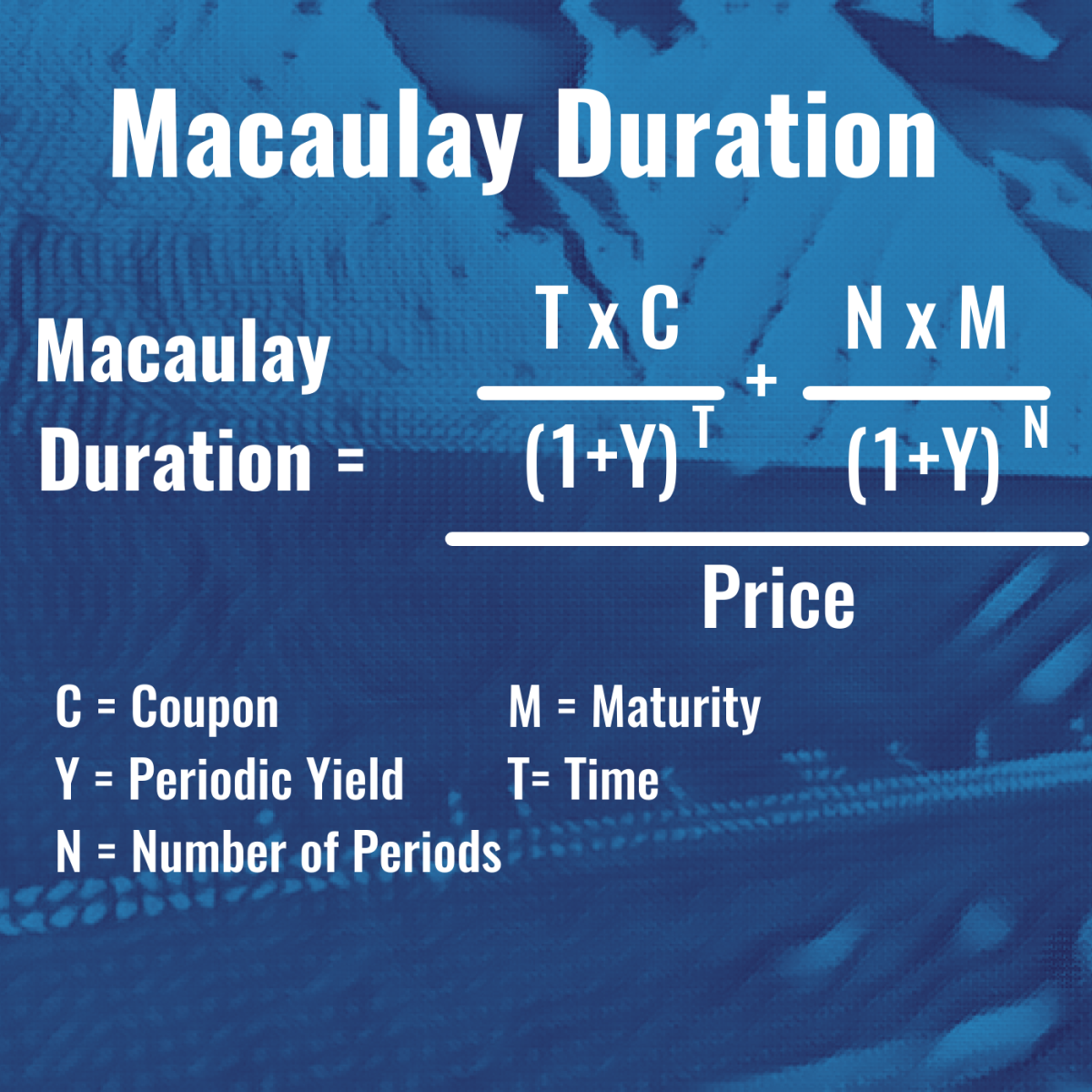

What is the duration of a bond? and How to Calculate It? The model calculates the time the present value of cash flows from a bond takes to realize. The simplified formula for Macaulay duration is as below: Macaulay Duration = Sum of PV of cash flows [PV (CF 1) + PV (CF 2) … + PV (CF n )] / Market price of the bond. See also Accounting for Issuance of Treasury Stock: Example, Journal Entries and More.

Duration and Convexity in Bond market

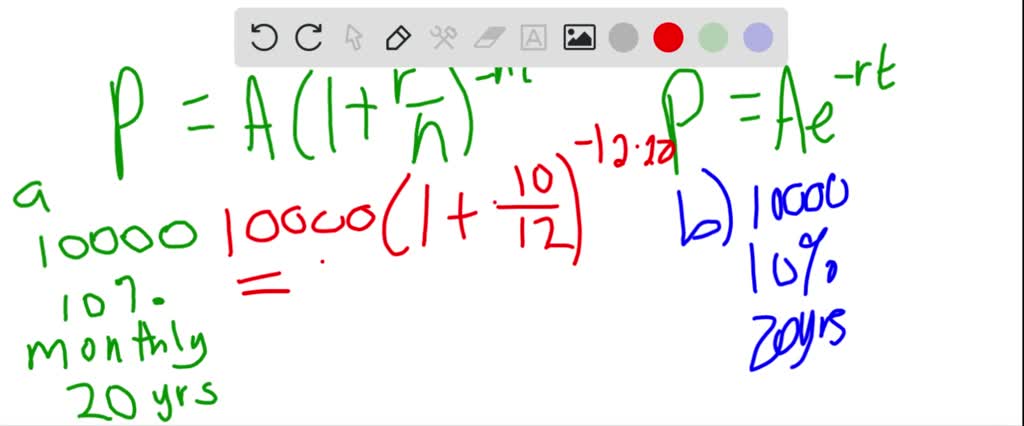

Solved a. What is the duration of a zero-coupon bond that - Chegg What is the duration of a zero-coupon bond that has five years to maturity? b. What is the duration if the maturity increases to 7 years? c. What is the duration if the maturity increases to 9 years? This problem has been solved! You'll get a detailed solution from a subject matter expert that helps you learn core concepts.

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

Duration and Zero Coupon Bonds - YouTube Examples of Macaulay duration are given for zero coupon bonds.

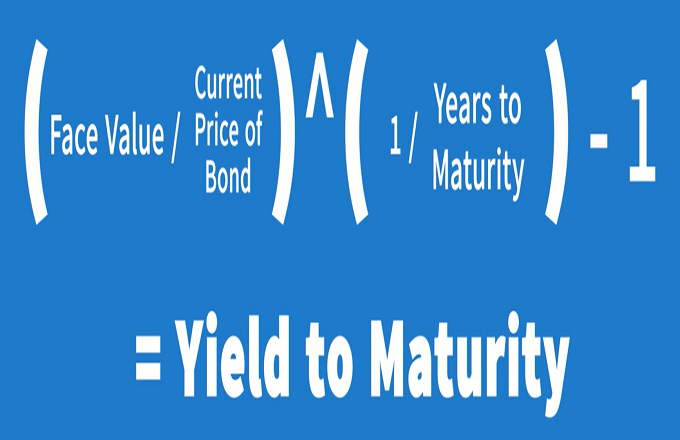

How Do I Calculate Yield To Maturity Of A Zero Coupon Bond?

Bond Duration - Investment FAQ For example, a 30 year bond with a 7% coupon and a 6% YTM has a duration of only 14.2 years. However, a zero will have a duration exactly equal to its maturity. A 30 year zero has a duration of 30 years. Keeping in mind the rule of thumb that the percentage price change of a bond roughly equals its duration times the change in interest rates ...

Zero Coupon Bonds Explained (With Examples) - Fervent ...

What is the Macaulay duration of a zero-coupon bond | Chegg.com Macaulay duration is the weighted average time to maturity of the cash flows received from a bond. With a zero-coupon bond, the Macaulay dur … View the full answer

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond . Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

![PDF] Duration and convexity of zero-coupon convertible bonds ...](https://d3i71xaburhd42.cloudfront.net/39b5487ce4f8becdfb0faf5ae6e30fd10537436c/13-Figure5-1.png)

PDF] Duration and convexity of zero-coupon convertible bonds ...

calculator.me › savings › zero-coupon-bondsZero Coupon Bond Value Calculator: Calculate Price, Yield to ... Instead interest is accrued throughout the bond's term & the bond is sold at a discount to par face value. After a user enters the annual rate of interest, the duration of the bond & the face value of the bond, this calculator figures out the current price associated with a specified face value of a zero-coupon bond.

SOLUTION: Duration of zero coupon bond - Studypool

Bond Duration Flashcards | Quizlet • The duration of a zero-coupon bond equals its time to maturity; • Holding maturity constant, a bond's duration is higher when the coupon rate is lower; ... • The zero-coupon bond has increased in value from $5000 to $5500 with the passage of time, and the duration is now 2 years. The perpetuity has paid a $500 coupon and remains worth ...

Macaulay's Duration, a Second Look - GlynHolton.com

Convexity of a Bond | Formula | Duration | Calculation - WallStreetMojo The duration of the zero-coupon bond which is equal to its maturity (as there is only one cash flow) and hence its convexity is very high While the duration of the zero-coupon bond portfolio can be adjusted as to that of a single zero-coupon bond by varying the nominal and maturity value of the zero-coupon bonds within the portfolio.

Zero Coupon Bond Value - Formula (with Calculator)

Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep If the zero-coupon bond compounds semi-annually, the number of years until maturity must be multiplied by two to arrive at the total number of compounding periods (t). Formula Price of Bond (PV) = FV / (1 + r) ^ t Where: PV = Present Value FV = Future Value r = Yield-to-Maturity (YTM) t = Number of Compounding Periods

Bonds of Mass Destruction - The Last Bear Standing

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

Solved a. What is the duration of a zero-coupon bond that ...

What Is Duration of a Bond? - TheStreet Definition - TheStreet

Zero-Coupon Bonds: Characteristics and Examples

Zero-Coupon Bond - an overview | ScienceDirect Topics

Finding YTM of a Zero Coupon Bond (6.2.1)

Trading zero-coupon bond with maturity T = 5 years. Average ...

Problems 63–66 involve zero-coupon bonds. A zero-coupon bond is a bond that is sold now at a discount and will pay its face value at the time when it matures; no interest payments are made. ...

Duration: Understanding the Relationship Between Bond Prices ...

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Duration Dv01 Maturity And Coupon A Graphical Analysis - Term ...

A default-free zero-coupon bond costs $91 and will pay $100 ...

Bond A is zero-coupon bond paying 100 one year from now. Bond B is a zero-coupon bond paying100 two years from now. Bond C is a 10% coupon bond that pays $10 one year from now and $10 plus the $100 ...

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents

Interest Theory Final – Time: 70 min

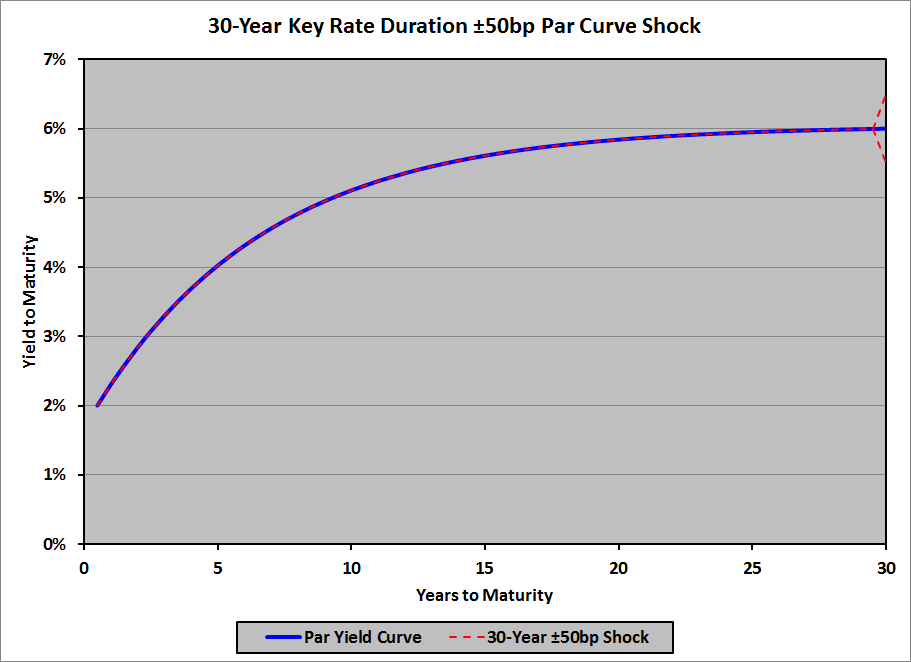

Key Rate Duration | Financial Exam Help 123

FRM: Dollar duration of zero coupon bond

What is the duration of a zero-coupon bond that has eight ...

Duration model

Modified duration of zero-coupond bond (FRM practice question)

Solved You are managing a portfolio of $1 million. Your ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

Post a Comment for "38 duration for zero coupon bond"